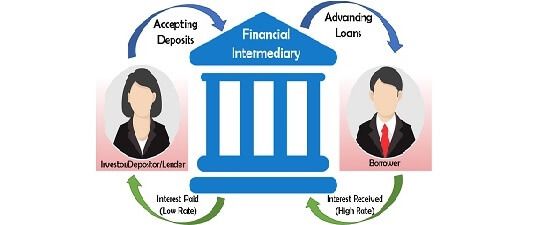

Banks play a crucial role as financial intermediaries in the economy, facilitating the flow of funds between savers and borrowers. Their role in financial intermediation involves several key functions that contribute to the efficient functioning of capital markets. Let’s explore the role of banks as financial intermediaries in the context of financial intermediation and capital markets.

- Mobilizing Savings: Banks gather funds from individuals, businesses, and other entities with surplus funds that are looking for a safe place to deposit their money. Through various deposit accounts, such as savings accounts and certificates of deposit (CDs), banks attract savings from the public. By mobilizing savings, banks provide a secure and convenient avenue for individuals to store their funds while earning interest.

- Providing Credit and Capital Allocation: One of the primary roles of banks is to provide credit to borrowers in need of funds. Banks evaluate the creditworthiness of borrowers and make loans to individuals, businesses, and governments. By allocating capital to borrowers, banks enable productive investments, entrepreneurship, and economic growth. They play a crucial role in evaluating credit risk, determining interest rates, and structuring loan terms.

- Liquidity Transformation: Banks engage in liquidity transformation by converting short-term, liquid deposits into longer-term loans. This process allows banks to provide liquidity to borrowers with longer-term investment needs while offering depositors the flexibility to withdraw their funds on demand. Banks manage this liquidity risk by maintaining a balance between their short-term liabilities (deposits) and long-term assets (loans).

- Risk Management: Banks assume and manage various risks in their role as financial intermediaries. They evaluate the creditworthiness of borrowers, assess the risk associated with loans, and establish risk management frameworks. Banks use risk mitigation techniques such as diversification, collateral requirements, and credit risk analysis to minimize the risk of loan defaults and protect depositors’ funds.

- Payment System Facilitation: Banks provide a secure and efficient payment system that enables transactions and facilitates economic activity. Through services such as checking accounts, debit cards, and electronic fund transfers, banks facilitate the movement of funds between individuals, businesses, and other entities. They play a critical role in ensuring the smooth functioning of the payment system, promoting economic transactions, and supporting commerce.

- Intermediation in Capital Markets: Banks also participate in capital markets by underwriting securities, facilitating initial public offerings (IPOs), and acting as intermediaries in the buying and selling of financial instruments. They provide services such as brokerage, investment advisory, and asset management to cater to the investment needs of individuals and institutional clients.

Overall, banks as financial intermediaries bridge the gap between savers and borrowers, mobilize savings, allocate capital efficiently, manage risks, and provide essential financial services to individuals and businesses. By performing these functions, banks support economic growth, facilitate investment, and contribute to the stability and development of capital markets.